Convenience stores in Australia - statistics & facts

Beyond the petrol pump, Australia’s service station-integrated shops and convenience-only stores (c-stores) provide busy, on-the-go consumers with a quick way to purchase food, beverages, grocery essentials, and other merchandise. Nonetheless, the country’s c-stores and ‘servos’ faced a challenging year in 2024, observing fluctuating non-discretionary consumer spending patterns due to rising fuel, food, and beverage prices. To drive in-store foot traffic and product sales, retailers stocking everyday essentials, ready-to-eat food, takeaway beverages, and ‘healthy’, functional product options in their shelf assortments, while investing in toilet amenities, EV charging stations, self-checkouts, diverse payment options, and loyalty programs, could stand out in Australia’s c-store crowd.

While tobacco retailing restrictions create a challenge for Australia’s c-stores, increased uptake in other categories like non-alcoholic beverages presents opportunity. With convenience, variety, and value fueling purchasing at c-stores, retailers prioritizing deals, everyday items, and trending categories could fare better in the coming years.

Popular convenience and fuel retailers

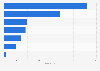

As of 2024, Australia had an extensive network of over 7,440 convenience stores. International chain 7-Eleven has captured significant market share in Australia, with over 750 7-Eleven stores nationwide. Other major convenience and petrol retailers operating in the country include Ampol (previously Caltex), BP, EG Group (in partnership with Ampol), Caltex (under Chevron), Woolworths Metro (with some co-owned by Ampol), and Viva Energy locations, including Reddy Express, OTR, and Liberty. Smaller, independent retailers include BP (under AA Petroleum), Metro Petroleum, APCO, New Sunrise (in partnership with various independent and chain service stations), NightOwl, United Convenience Buyer (UCB) member stores like fast&ezy, and United Petroleum, among others.Will Australia’s new tobacco laws impact c-stores?

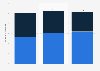

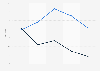

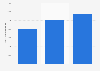

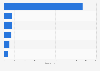

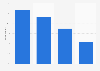

Australia’s c-store product sales exceeded 10 billion Australian dollars in 2024, with the food and beverages segment continuing to pull ahead of non-food. While tobacco remains a high-value convenience product category, making up around 25 percent of sales in 2024, the category’s contribution has significantly decreased from almost 35 percent share in 2022. Furthermore, under new regulations commencing July 1, 2025, all cigarettes and other nicotine-containing goods sold nationwide must comply with reformed taxation rules, packaging and sizing specifications, and advertising regulations. Moreover, certain tobacco products will no longer be available, including menthol cigarettes and accessories. These changes will likely shrink Australia’s c-store tobacco sales further due to reduced product availability and visibility, alongside possible price rises following tax increases.Which c-store categories are thriving?

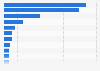

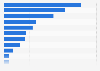

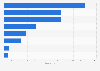

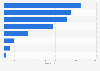

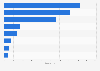

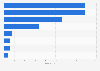

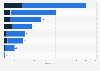

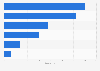

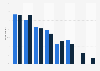

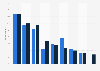

Packaged beverages, foodservice, confectionery, hot drinks, and snack foods remain Australia’s key c-store categories besides tobacco. In 2024, packaged beverages stole tobacco’s crown to become the country’s leading convenience category, with consumers quenching their thirst with drinks ranging from international brands like Pepsi to local offerings such as Bundaberg Ginger Beer. The ‘grab-and-go’ foodservice and hot takeaway beverage categories are also heating up as consumers increasingly search for convenient and affordable restaurant and café-style meals and hot brews. Additionally, snack foods and confectionery remain a cornerstone of Australian convenience retailing, with demand for ‘healthy’ options rising. According to a 2024 survey, among shoppers purchasing convenience products alongside fuel, hot drinks, particularly coffee, and cold beverages were the most prevalent purchases. Among convenience-only consumers, cold drinks were the most popular. While younger generations’ convenience purchases focused on cold beverages and snacks, 40- to 59-year-olds favored hot drinks, and newspapers or magazines were the best-selling among those 60 years and over.While tobacco retailing restrictions create a challenge for Australia’s c-stores, increased uptake in other categories like non-alcoholic beverages presents opportunity. With convenience, variety, and value fueling purchasing at c-stores, retailers prioritizing deals, everyday items, and trending categories could fare better in the coming years.